Shopping for a car in the U.S. can be both exciting and overwhelming, especially if your credit history is nonexistent.

This article aims to help anyone new to credit—such as recent immigrants, college students, or young professionals—understand how car financing with no credit in the U.S. works, and how to approach the process with realistic expectations.

Perhaps you’re wondering how lenders might view your application, or how to avoid expensive mistakes. Here’s what matters most and why staying informed can make a significant difference.

Why Is Credit Important for Car Financing in the U.S.?

Credit history acts like a financial report card for lenders. When you apply for an auto loan, most banks or dealerships want to assess your ability to pay back the money.

Without any credit record, lenders lack the information they typically use to determine risk. This can make approval more challenging, but not impossible. More Americans each year find themselves in similar situations, so you’re not alone.

For many, building credit starts with one challenging purchase—sometimes, it’s their first car.

Common Challenges of No Credit Car Loans

Higher Interest Rates

A lack of credit usually means higher interest rates. Since lenders don’t have your past borrowing habits, they offset this uncertainty by charging more. The difference can add up over the years.

It’s not unusual to see interest rates that are several percentage points higher than those offered to borrowers with established credit. Prospective car buyers might experience a moment of sticker shock here.

But sometimes, waiting until you’ve built even a thin credit file might save you money in the long run.

Upfront Payment Requirements

Lenders may ask for larger down payments from applicants without credit history. The idea is simple: a bigger initial investment reduces their risk if things don’t go as planned.

This upfront cost can be a barrier, especially for students or newcomers who have limited savings. Saving for a larger down payment before seeking financing might improve approval odds or lead to slightly better loan terms.

Limited Vehicle Choices

Some lenders, especially those specializing in so-called “no credit car loans,” might only approve certain makes or models—usually vehicles that retain value well or are easy to repossess.

This can limit personal preference and push buyers toward older models or vehicles with fewer features, which isn’t always the most comfortable outcome.

Yet, some prefer starting with something modest and upgrading later, once their credit opens more possibilities.

Best Options for Car Financing Without Credit

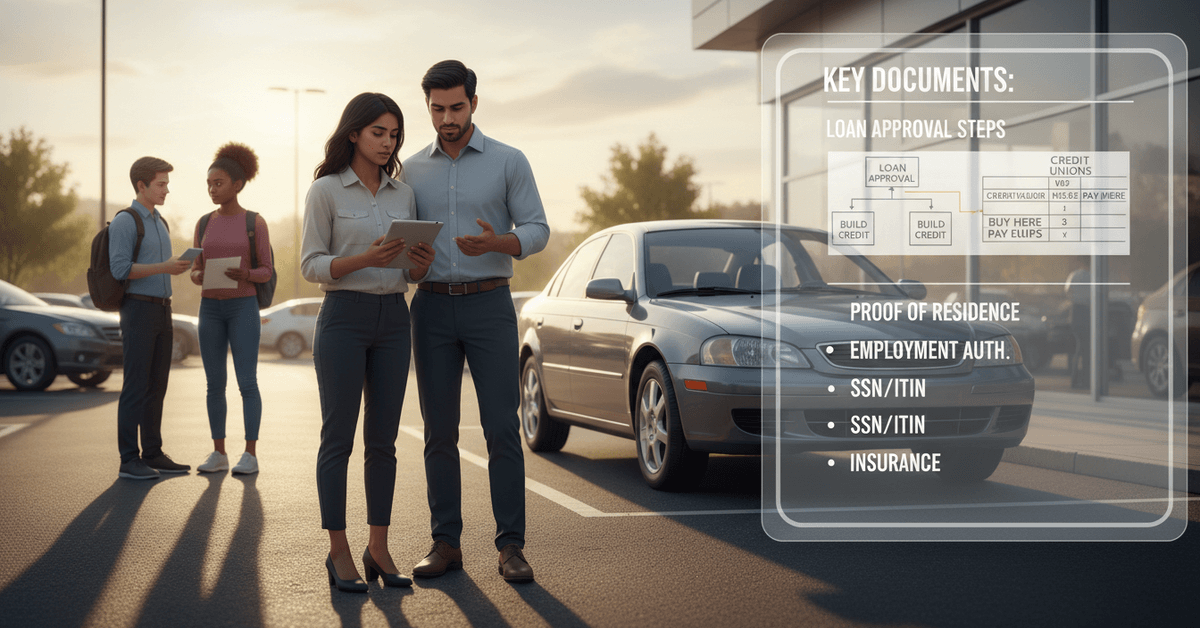

Credit Unions and Community Banks

Credit unions are often more flexible than major banks, particularly for new borrowers. As member-owned organizations, they sometimes consider alternative factors, like employment stability or community involvement, when making lending decisions.

Applicants may find greater understanding at credit unions and community-focused banks, especially when a face-to-face relationship exists.

Subprime Lenders and Buy Here Pay Here Dealerships

“Buy Here Pay Here” dealers specialize in financing people with little or no credit. While convenient, interest rates and fees are usually higher, and loan terms less flexible.

It can help to compare several options, as offers—and their fine print—do vary. While these dealerships sometimes have a poor reputation, some buyers find them accessible in a pinch.

Co-Signers: A Help or a Hassle?

A co-signer with established credit may help secure a better loan for those without credit. This person agrees to pay if you can’t, which can reassure lenders.

The flip side is, there’s a risk for both parties. If payments are missed, both credit scores can suffer. Some friends or family members hesitate, understandably.

Online Fintech Platforms

Certain online lenders now use alternative data, such as employment, education, or even rental history, for making decisions. These options often serve those who don’t fit traditional profiles.

Searching for ” car loans for no credit history ” can bring up several fintech providers with relatively transparent terms and online applications, which suits those comfortable handling things digitally.

Proven Strategies to Improve Approval Chances

Save for a Larger Down Payment

Any extra money for the initial payment reduces the loan size and the risk from the lender’s perspective. Sometimes, this unlocks approvals that might not be available otherwise.

Even a seemingly small increase in down payment may tip things in your favor or result in a lower rate. Starting a dedicated car fund in advance might be worth considering, especially if credit building will take time.

Choose a Modest or Used Vehicle

Financing a less expensive car reduces the lender’s risk. In many cases, affordable used cars are easier to get loans for if you have no credit.

While it might not be your dream car, a practical purchase now can help set up better borrowing terms in the future. Sometimes, patience does pay off. It’s a learning curve many have experienced.

Gather Proof of Income and Residency

Lenders still need to see some evidence of your ability to make payments. Recent pay stubs, tax returns, or a letter from your employer can support your application.

Evidence of stable residency (like utility bills in your name) can also reassure lenders. Being prepared with these documents might make the application smoother, if nothing else.

Consider Alternative Credit Data

Some lenders allow you to submit utility or cell phone payment records as evidence of reliability. This isn’t universally accepted, but fintech and newer lenders are increasingly open to it.

Sometimes, there’s a little extra paperwork involved, but for people with consistent bill payments—even if nothing appears on traditional credit reports—this can be a useful workaround.

Building Your Credit for Future Car Financing

Open a Secured Credit Card

It may be helpful to start building credit even before or alongside your auto loan. Secured credit cards require a cash deposit but report monthly payments to credit bureaus.

Regular, on-time payments, even with minimal monthly spending, can begin to establish a positive credit record. Over time, this might qualify you for better car loan terms.

Become an Authorized User

Asking to be added as an authorized user on someone else’s credit card can help you inherit some of their credit history. It’s a small step, but lenders do sometimes consider it.

Of course, this relies on the primary cardholder’s responsible usage. If their payments are late, your credit can suffer too.

Legal, Tax, and Documentation Requirements

Required Documentation for Non-Citizens

Immigrants or non-U.S. citizens may face extra documentation requirements. Lenders commonly ask for proof of legal residence, employment authorization, and a Social Security Number or ITIN.

Proof of income and residency still play a significant role, just as they do for citizens. For the latest requirements, it might help to check with your local Department of Motor Vehicles or an attorney.

Understanding Loan Terms and Total Cost

Always review the loan agreement for interest rates, total repayment amount, and the existence of prepayment penalties. It’s easy to focus on monthly payments, but the true cost is the sum paid over the entire loan.

Some buyers get caught off guard when they realize how much interest they’re paying in the end. Double-checking the math can help avoid surprises.

Insurance and Registration

Car loans typically require proof of insurance and a registered vehicle. Lenders need assurance their investment is covered by auto insurance.

Be ready to shop for insurance quotes at the same time as financing—rates can vary widely, especially for new drivers or recent arrivals. This is one of those oft-overlooked expenses that can affect affordability.

Frequently Asked Questions about Car Loans and No Credit

Is It Possible to Get a Zero-Interest Loan with No Credit?

This is extremely rare. Most interest-free promotions require good or excellent credit. It’s good to be skeptical of offers that promise the impossible.

How Long Does It Take to Build Enough Credit for Better Loan Terms?

Some see improvements in as little as six months, but most lenders prefer at least one year of positive credit behavior. The process can feel slow—but it does work, gradually.

Does Applying for Several Loans Hurt My Score?

Each loan application typically causes a small, temporary dip in your score, but rate-shopping within a two-week period is often treated as a single inquiry. Overdoing it, though, can be a red flag.